Back to industries

Buy Now Pay Later for Commercial Furniture

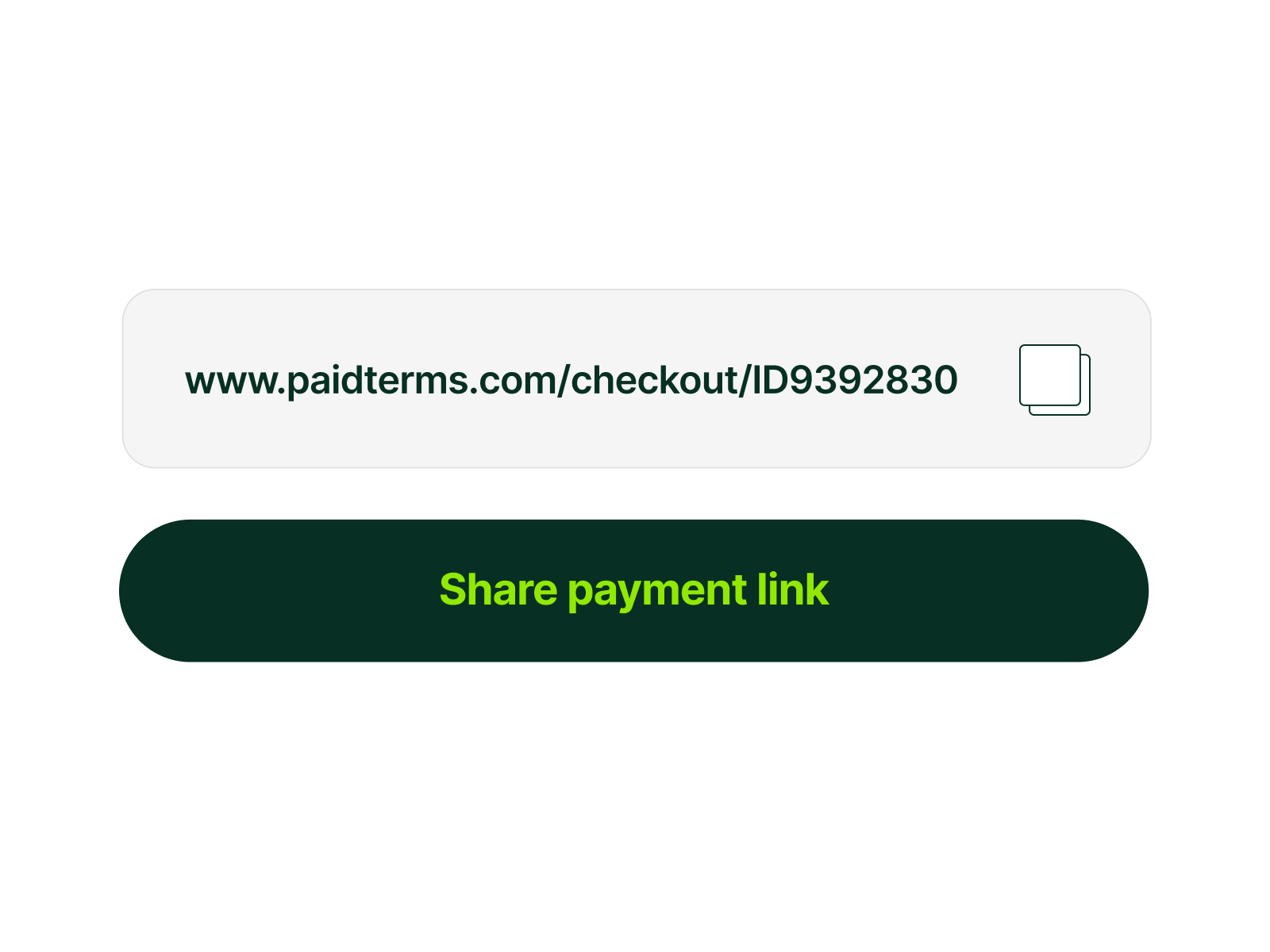

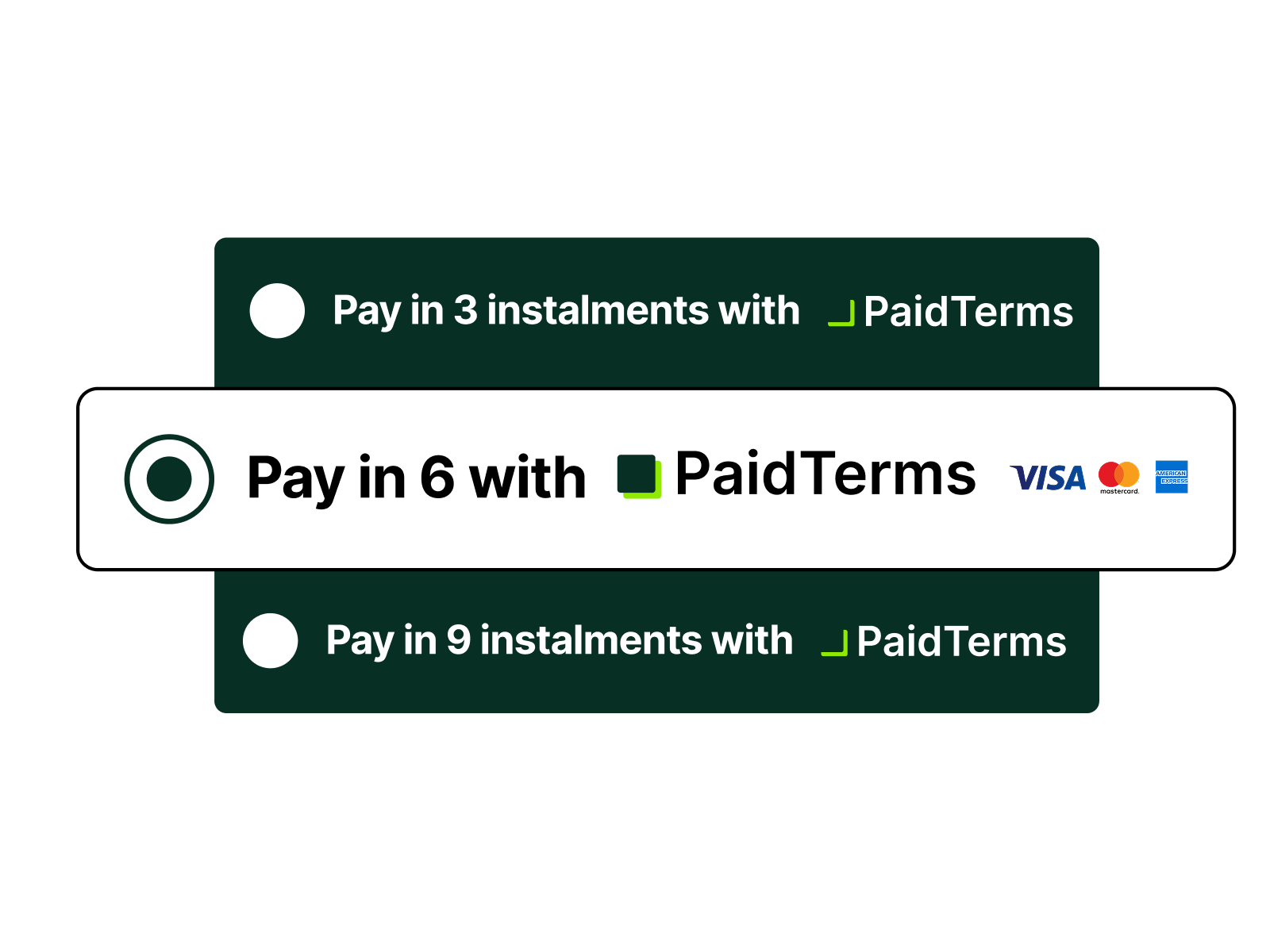

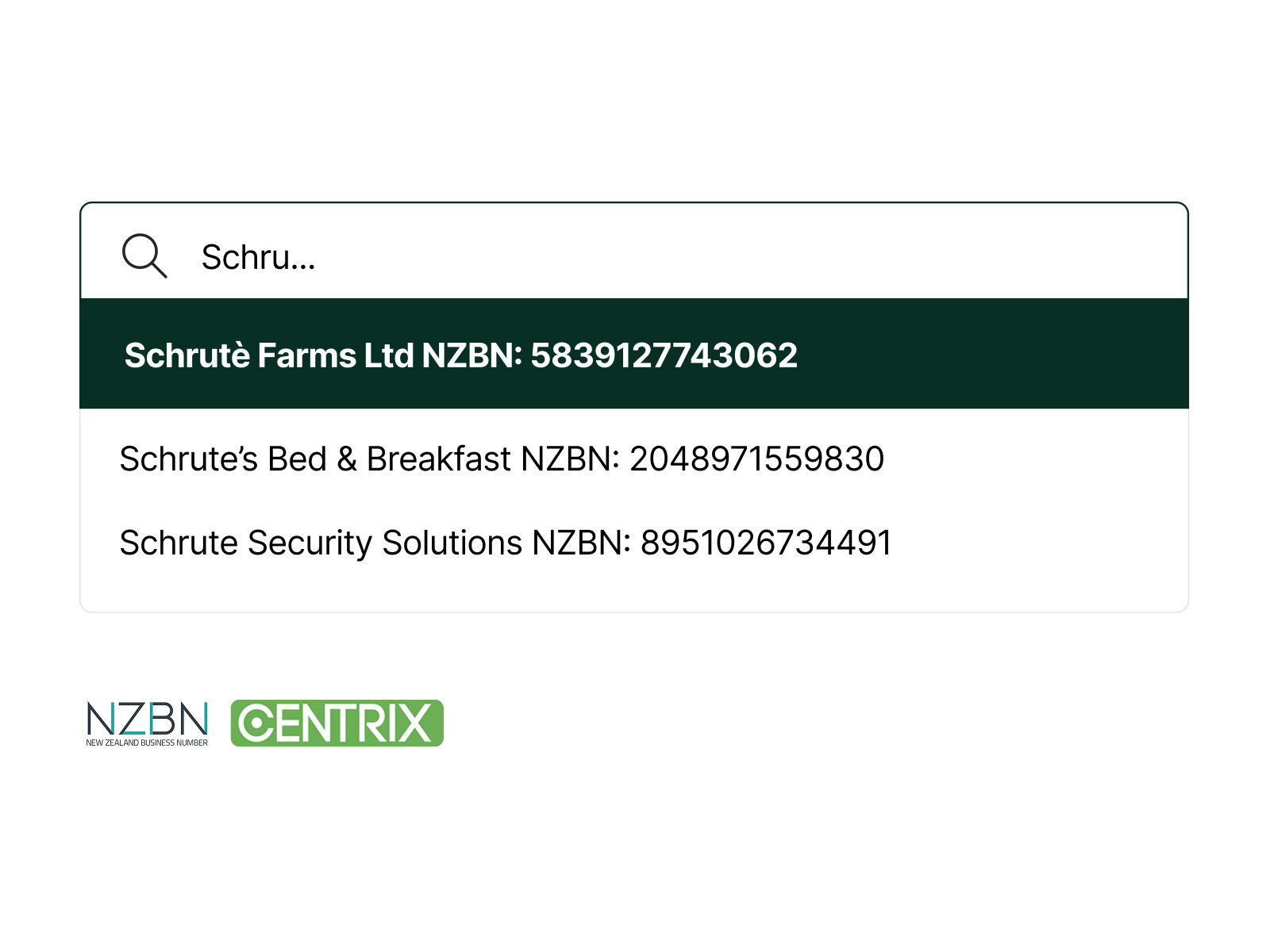

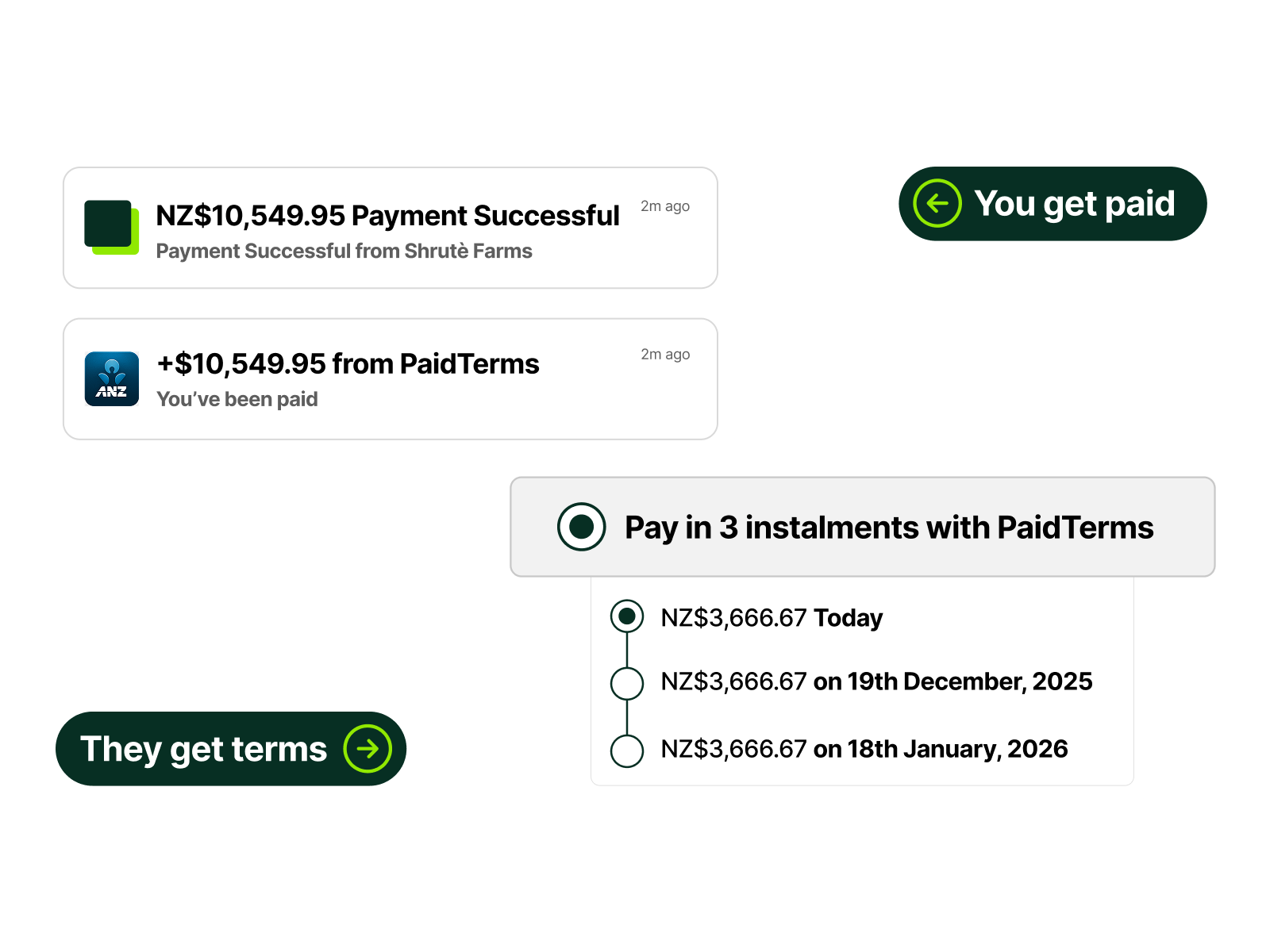

We help commercial furniture businesses offer instalments, so buyers can spread the cost of fit-outs and large orders while you get paid upfront with less risk and admin.