Back to industries

Buy Now Pay Later for Plastic Injection Moulding

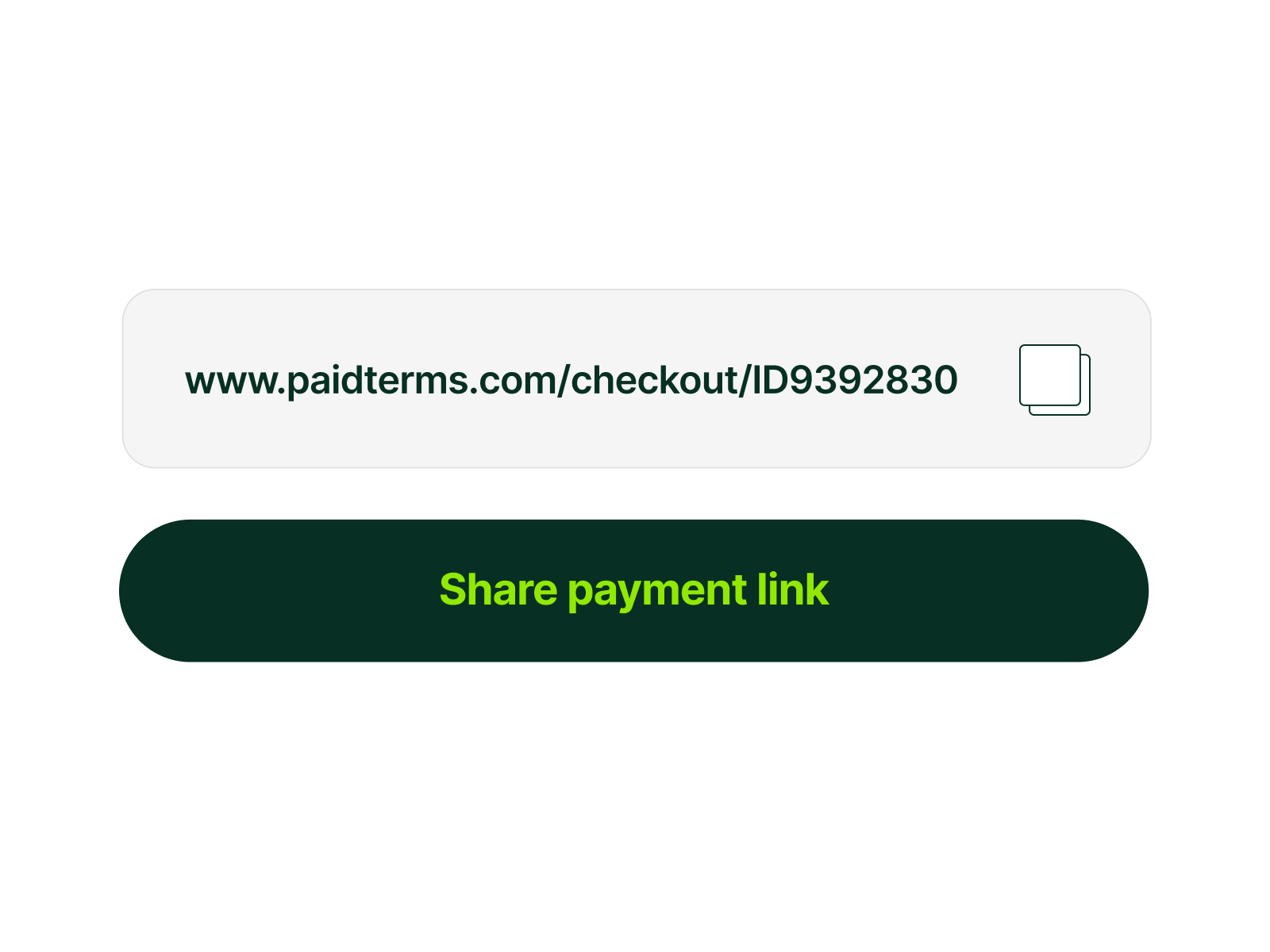

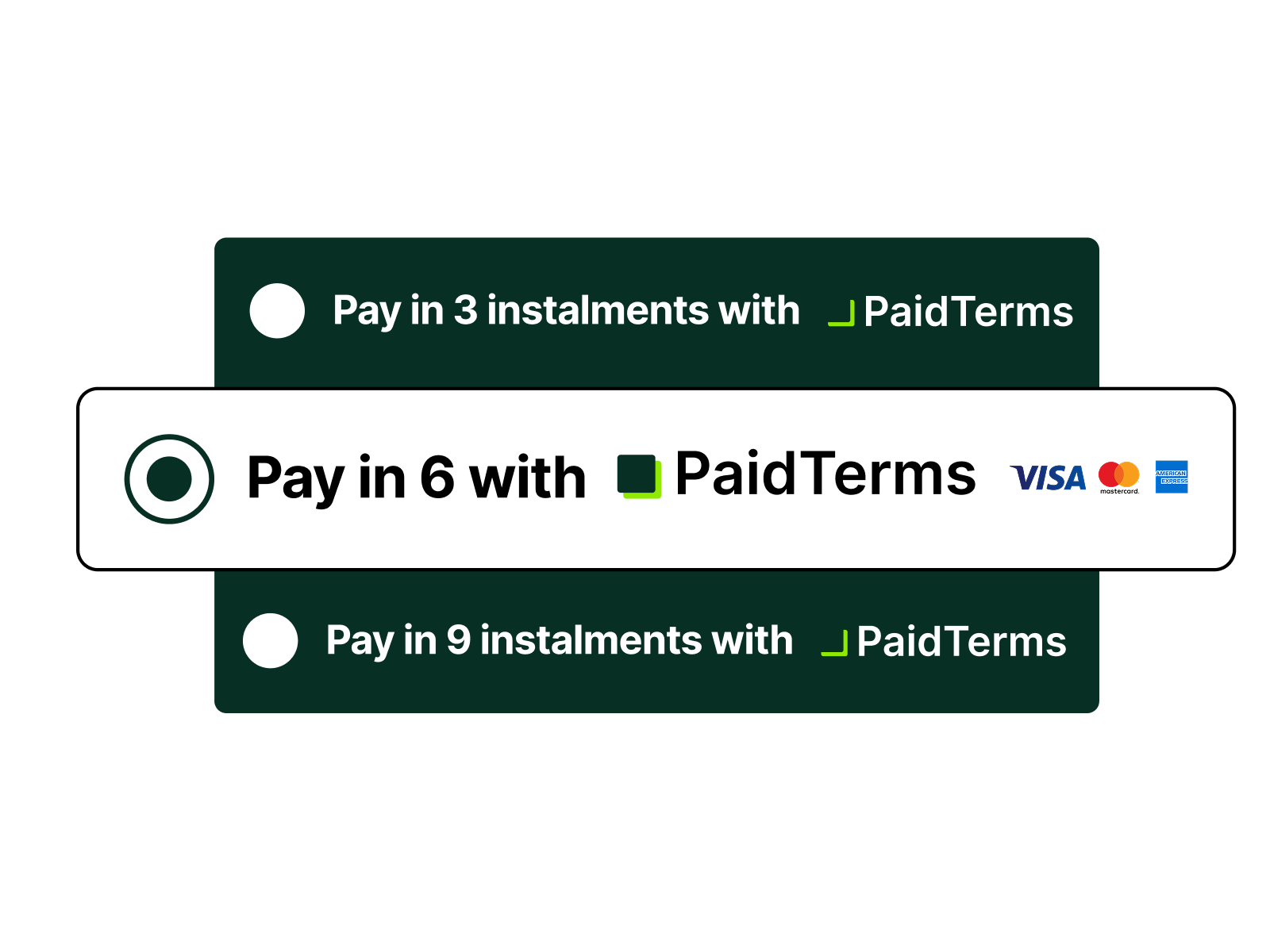

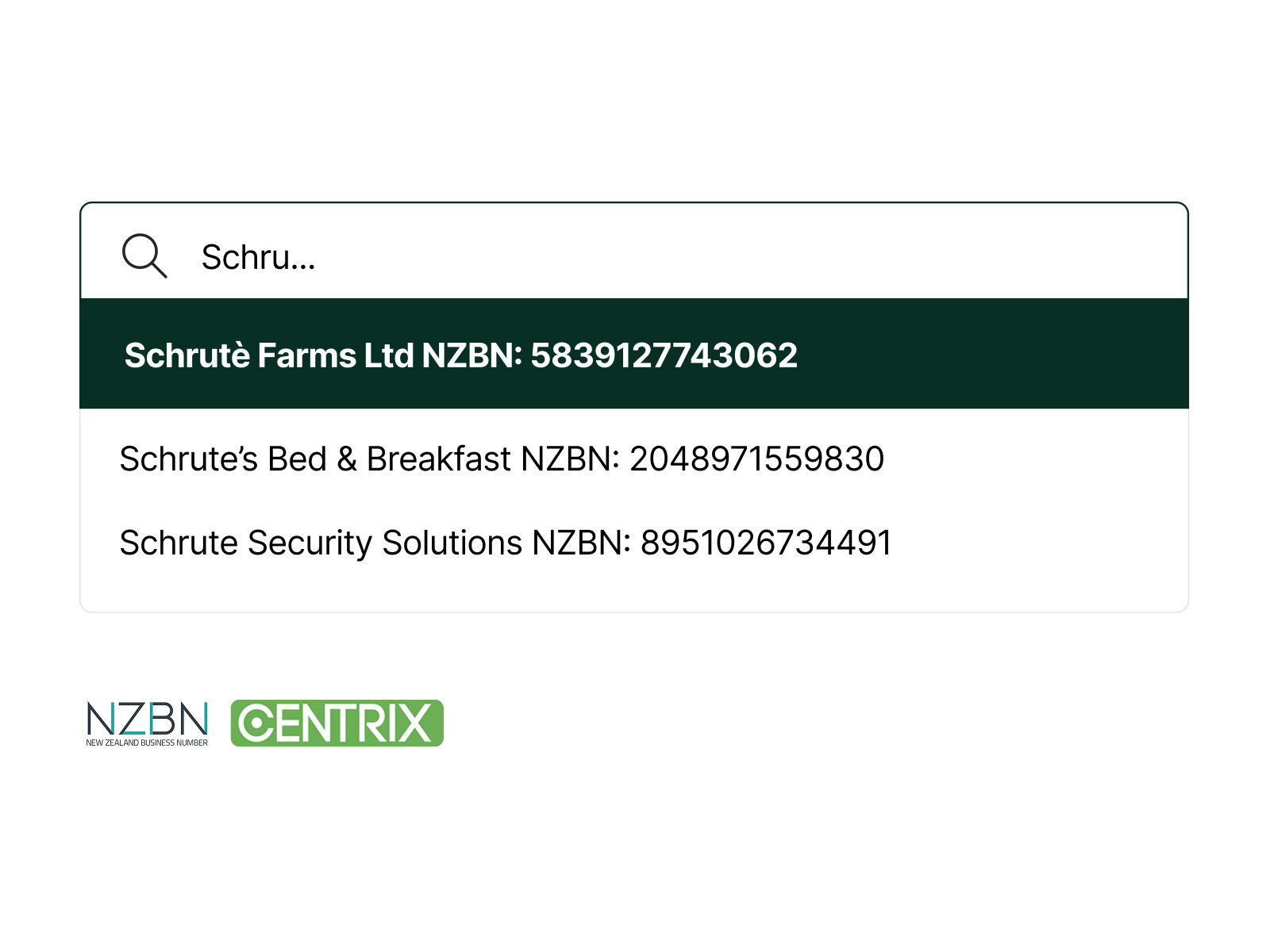

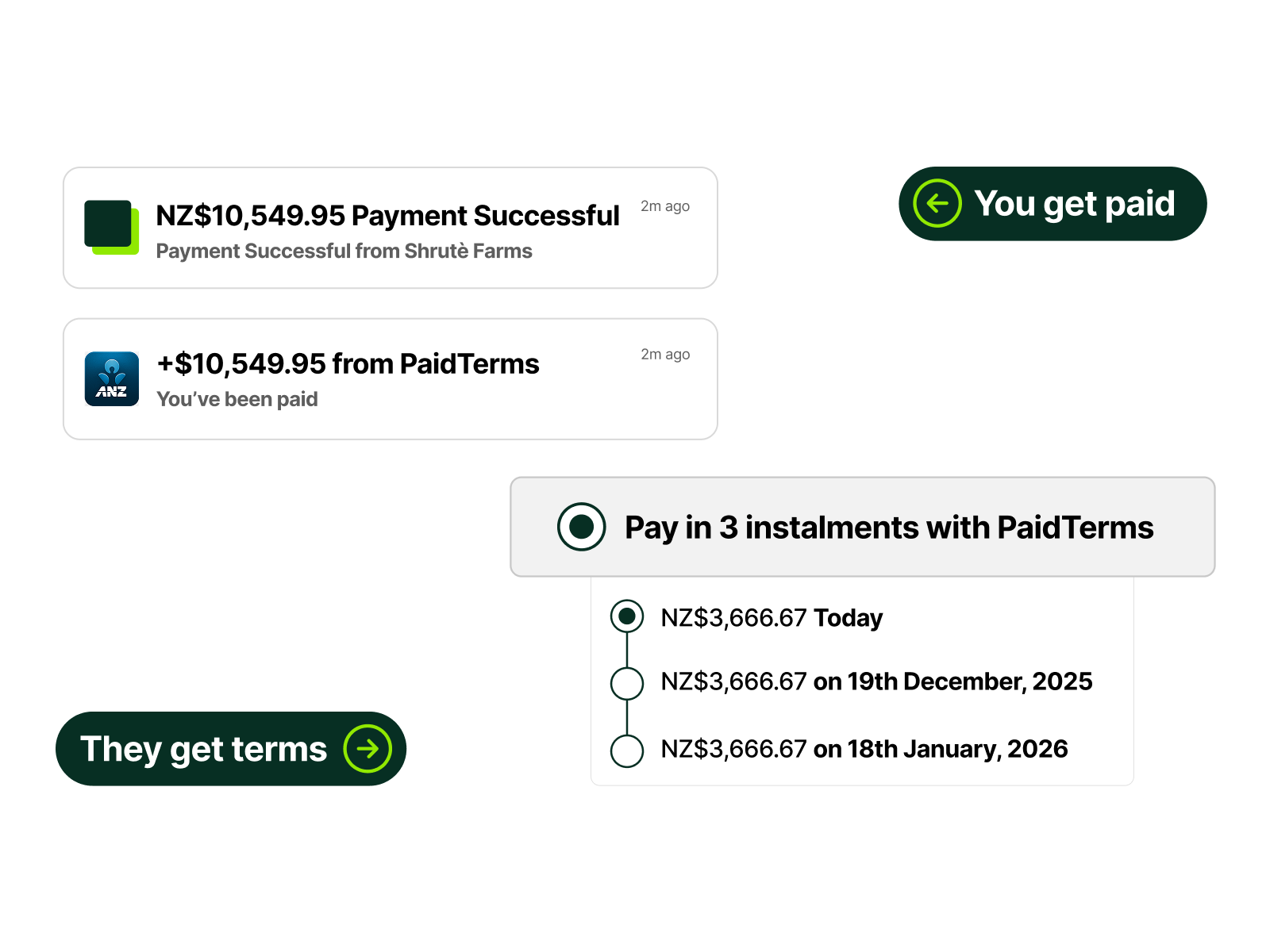

We help injection moulding companies offer flexible payment terms to product manufacturers and OEMs, enabling larger production runs while you get paid upfront with reduced credit risk.