Buy Now Pay Later for Food & Beverage Manufacturers

We help food and beverage businesses offer instalments, so buyers can spread costs while you get paid upfront with less risk and admin.

Why Food & Beverage Manufacturers Use Instalments

Enable larger ingredient and production orders while protecting your cash flow and eliminating credit risk.

Buyers commit to bigger ingredient and product runs when they can spread costs over time

Producers need to stock up ahead of peak seasons without depleting working capital

Standard 30–60 day terms create cash flow gaps that limit growth and reordering

Win more supply contracts by offering flexible payment options competitors don't

How it works

Get set up in minutes and start offering instalments on your next invoice.

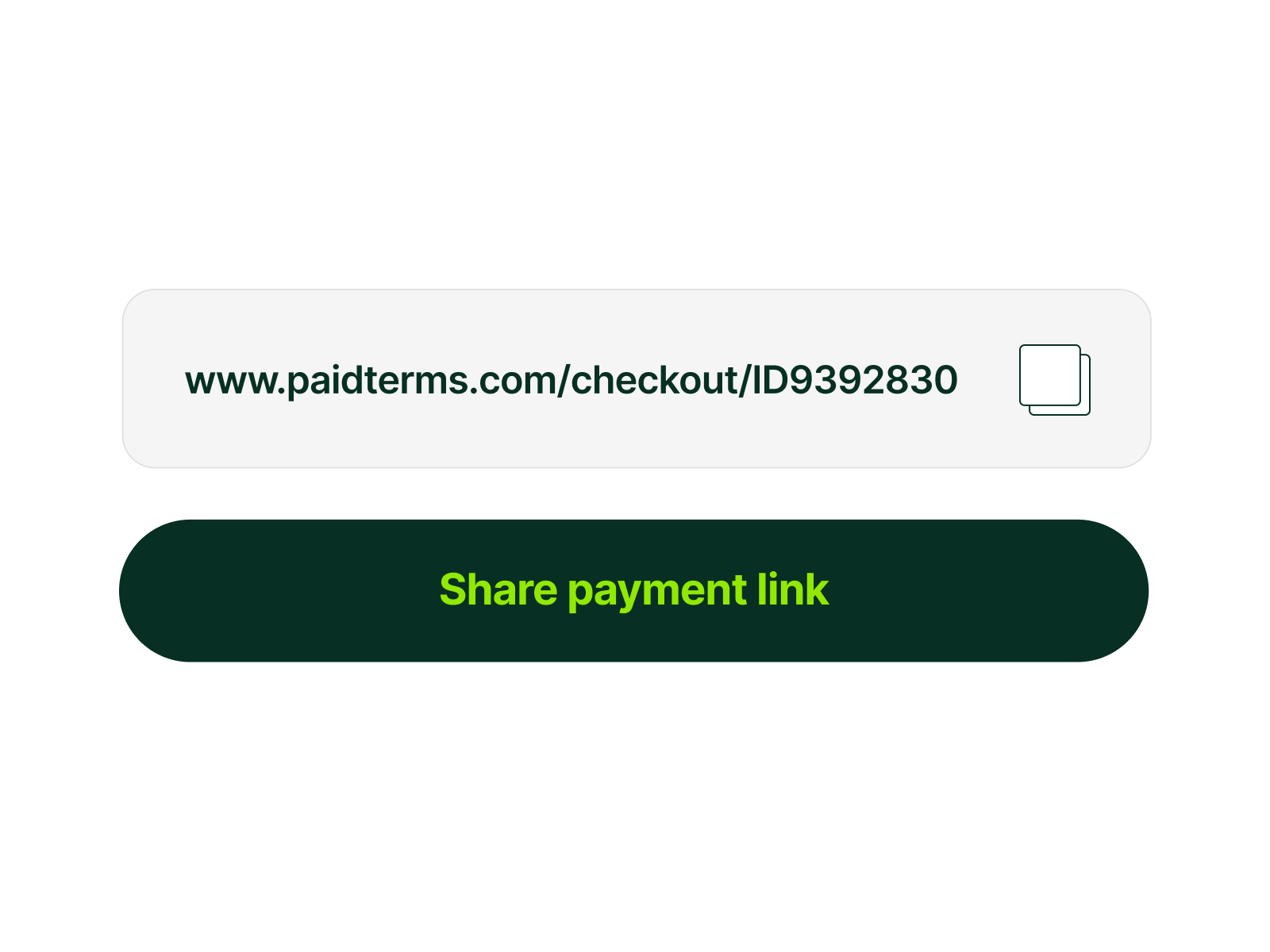

We give you a designated payment link to send to customers. Add it to your invoice email and let the buyer choose terms.

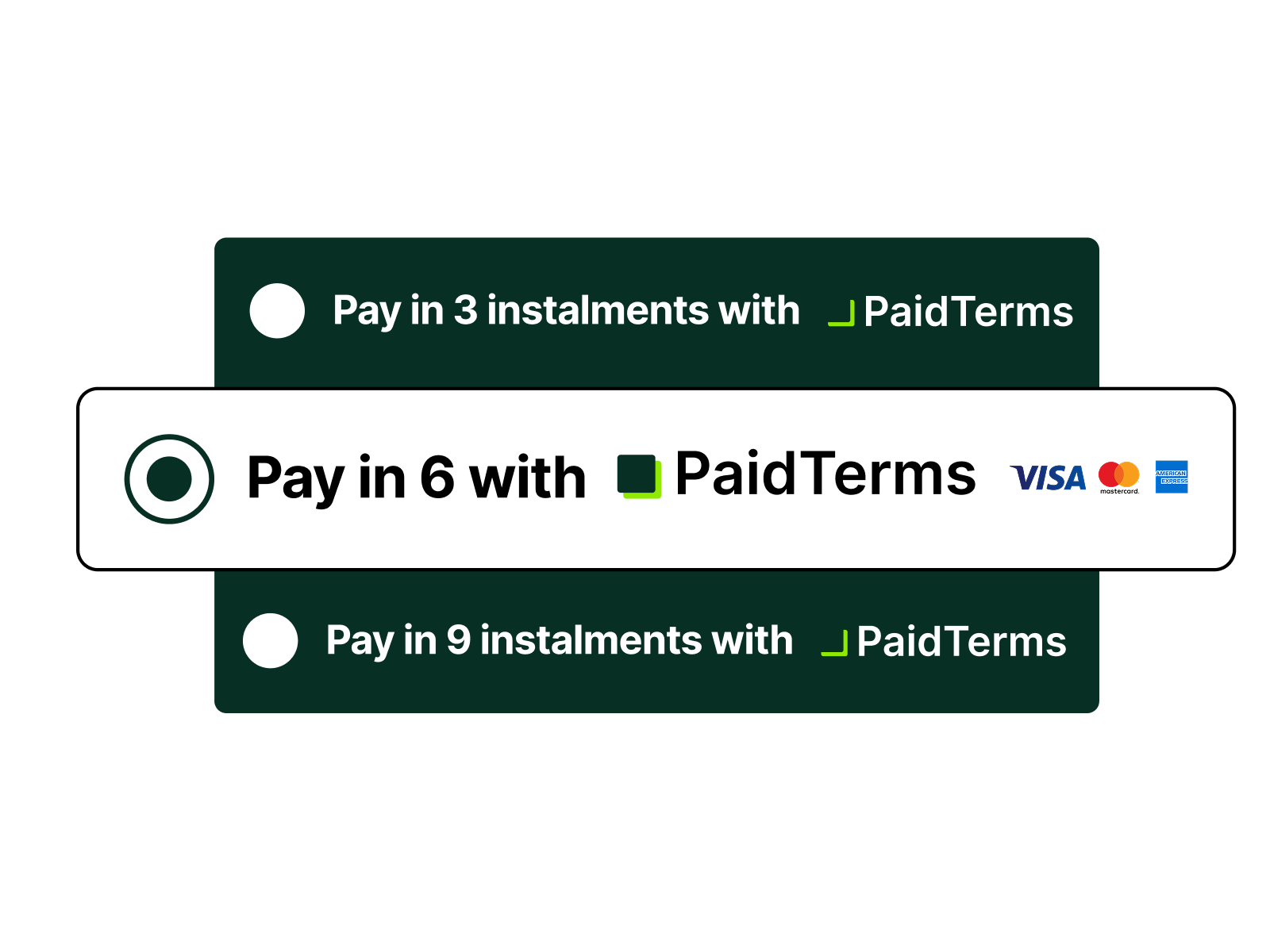

Your customer can split the invoice into 3, 6, 9, or 12 monthly instalments at checkout.

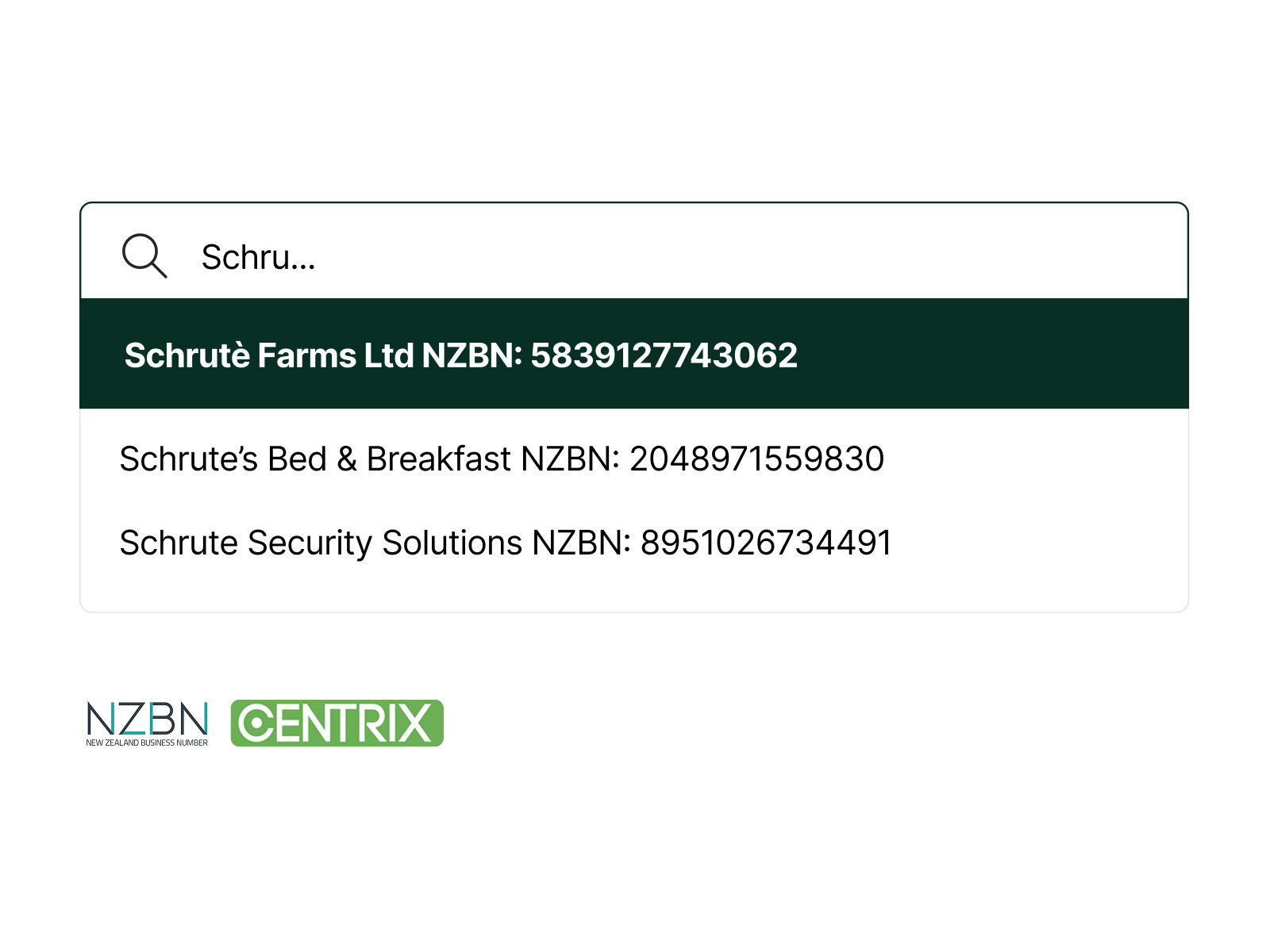

PaidTerms runs a quick business check using NZBN and Centrix to confirm the buyer's details and approve the transaction.

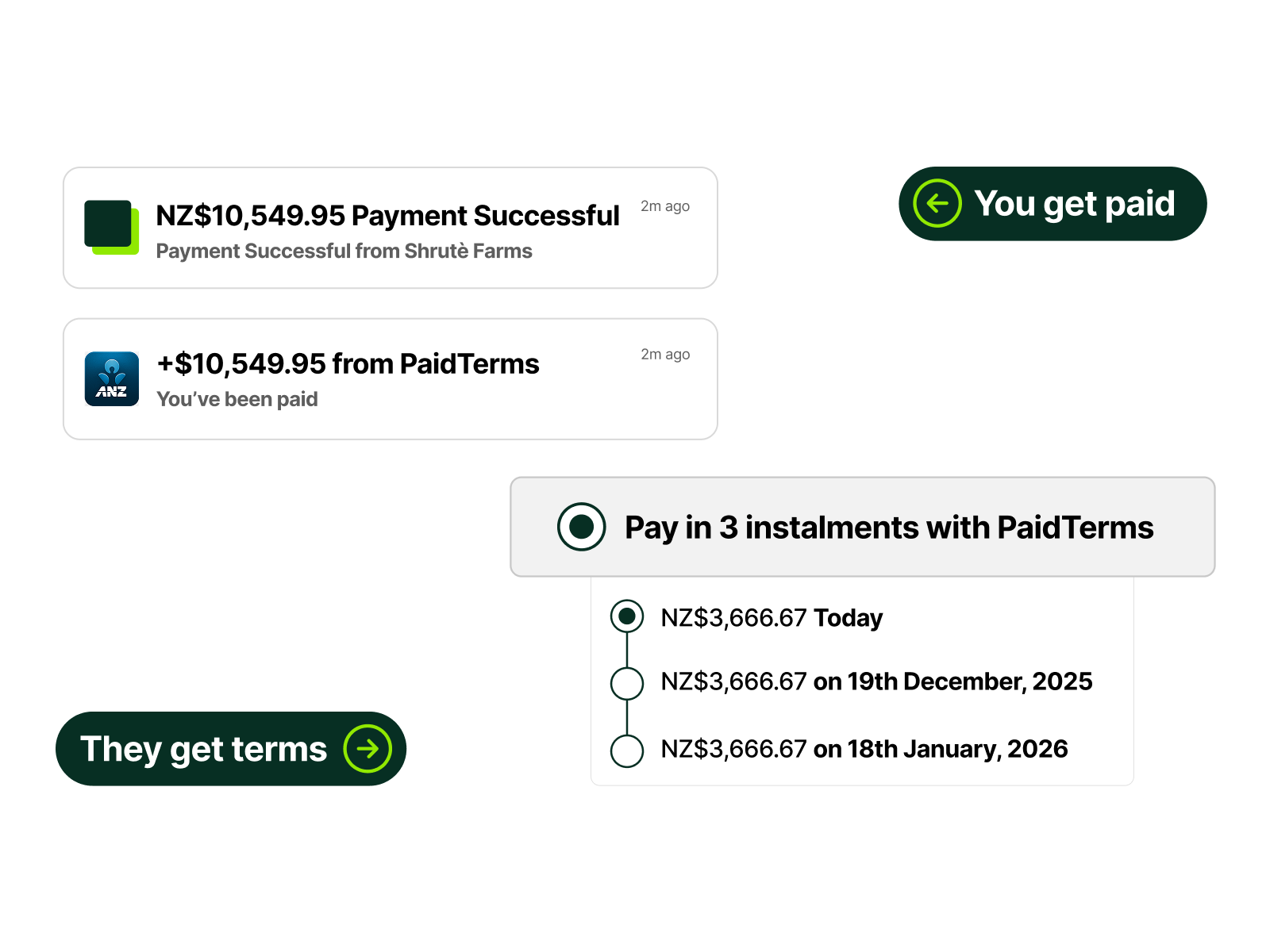

You receive the full invoice amount upfront, and your customer pays it off in instalments through PaidTerms.

Example: Food & Beverage Order Using Instalments

See how the same scenario plays out differently

Buyer Type

Beverage brand scaling up ahead of peak summer demand

Order Size Needed

$38,000 for full ingredient and packaging run

- Buyer splits order into smaller monthly batches

- Higher per-unit costs from smaller runs

- Stock runs out mid-season, missing peak sales

- Supplier loses revenue to a more flexible competitor

- Buyer commits to full $38,000 order upfront

- Pays in manageable instalments across the season

- Supplier receives $38,000 upfront

- Brand is fully stocked and ready for peak demand