Help Your Skincare Clients Say Yes to Bigger Orders

We help skincare and cosmetics manufacturers offer instalments to their brand clients, so buyers can commit to larger production runs while you get paid upfront with less risk and admin.

Why Skincare & Cosmetics Manufacturers Use Instalments

Help your brand clients commit to larger production runs while you get paid upfront and eliminate credit risk.

Brand clients approve bigger manufacturing orders when they can spread the upfront cost rather than paying in full on placement

Indie and emerging brands struggle to meet minimum order quantities — instalments remove the cash barrier and unlock the full run

Brand clients won't see revenue until product hits shelves — instalments let them commit to production before cash comes in

Win more contract manufacturing clients by offering flexible payment terms that competing manufacturers don't

How it works

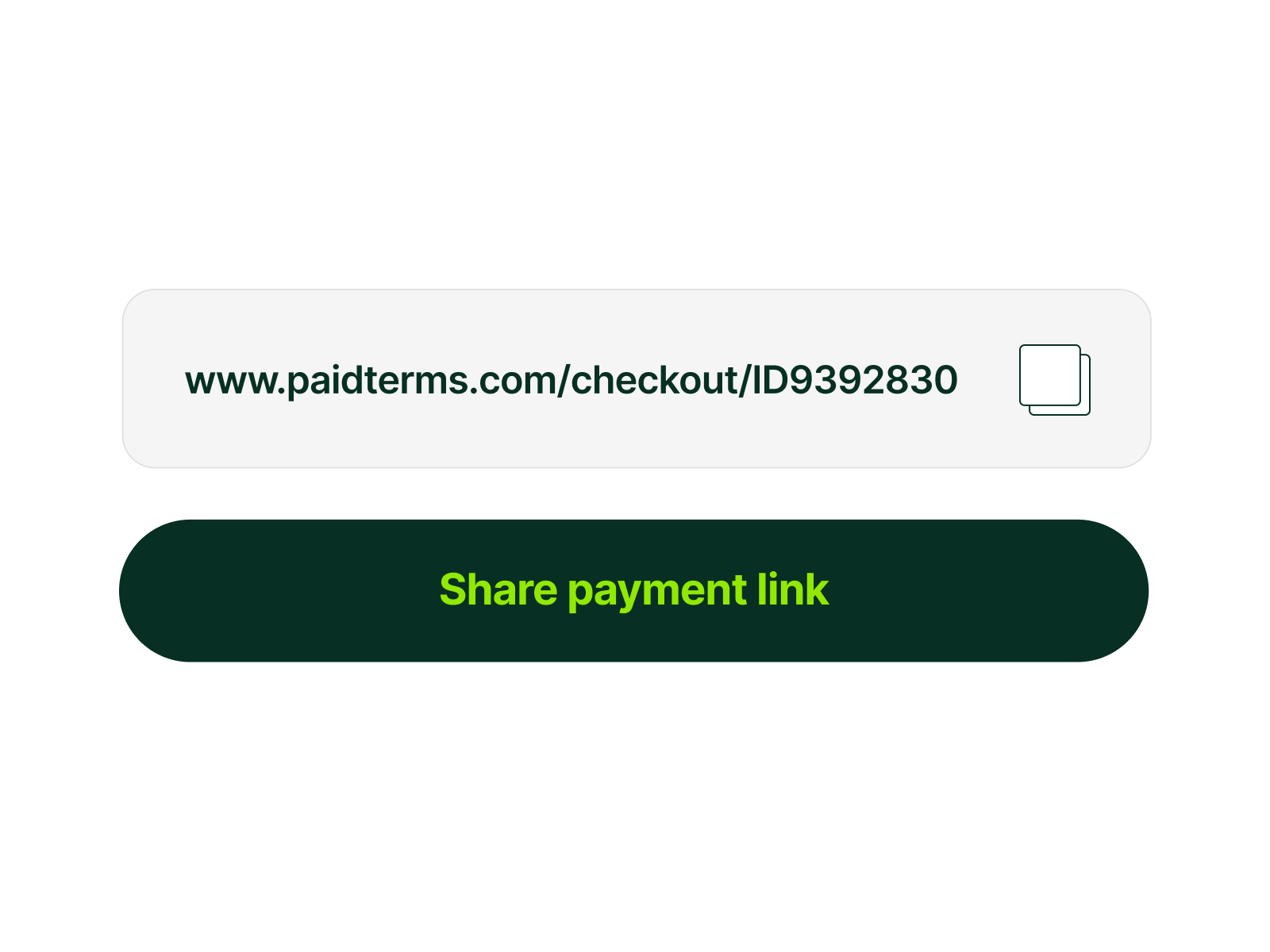

Add your customer's details and invoice amount. PaidTerms generates a secure link you can drop straight into your invoice email — no integrations required to get started.

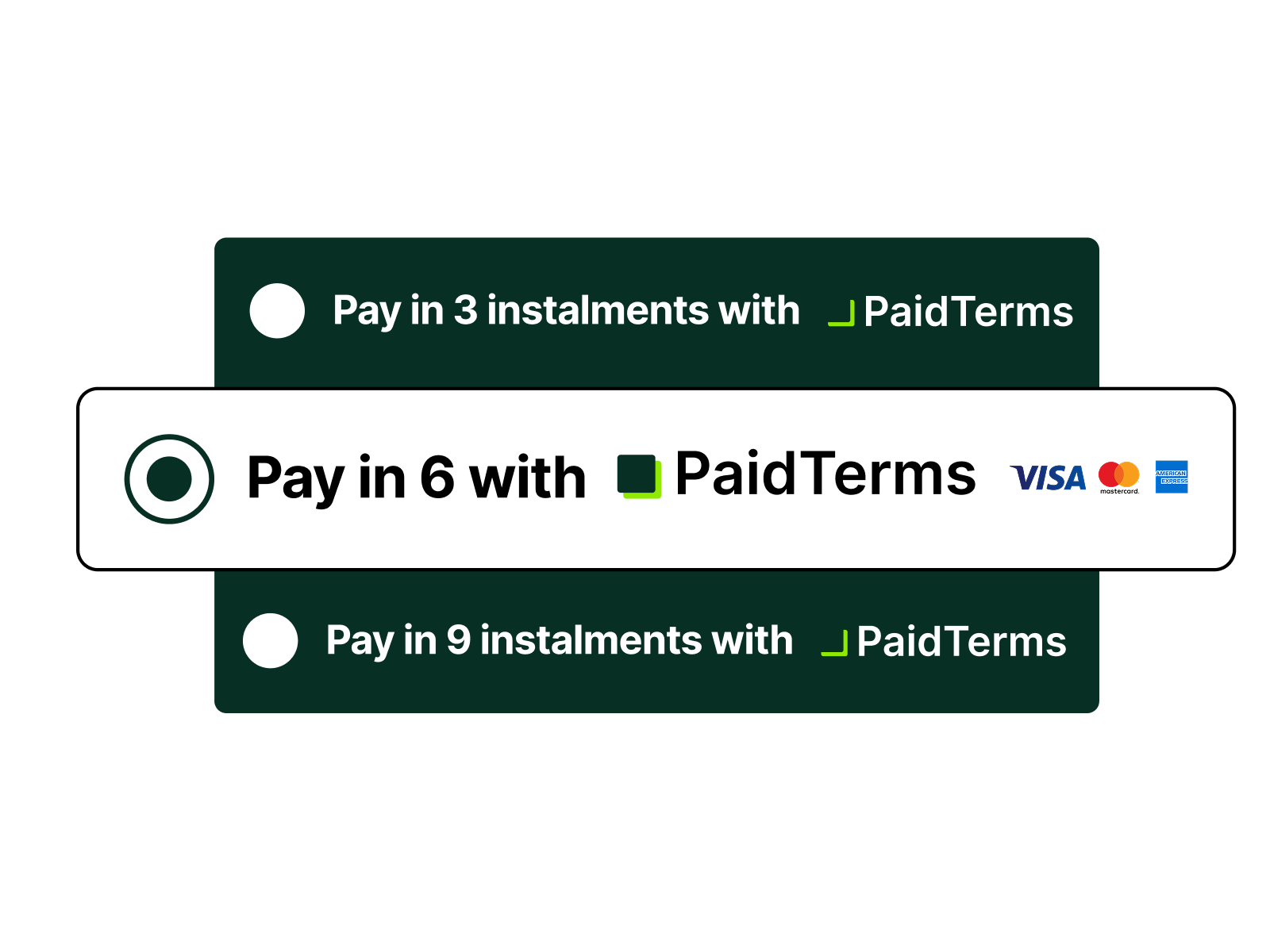

Your customer clicks the link, picks 3, 6, 9, or 12 monthly payment terms, and confirms their plan. Done in under two minutes — no paperwork, no director guarantees.

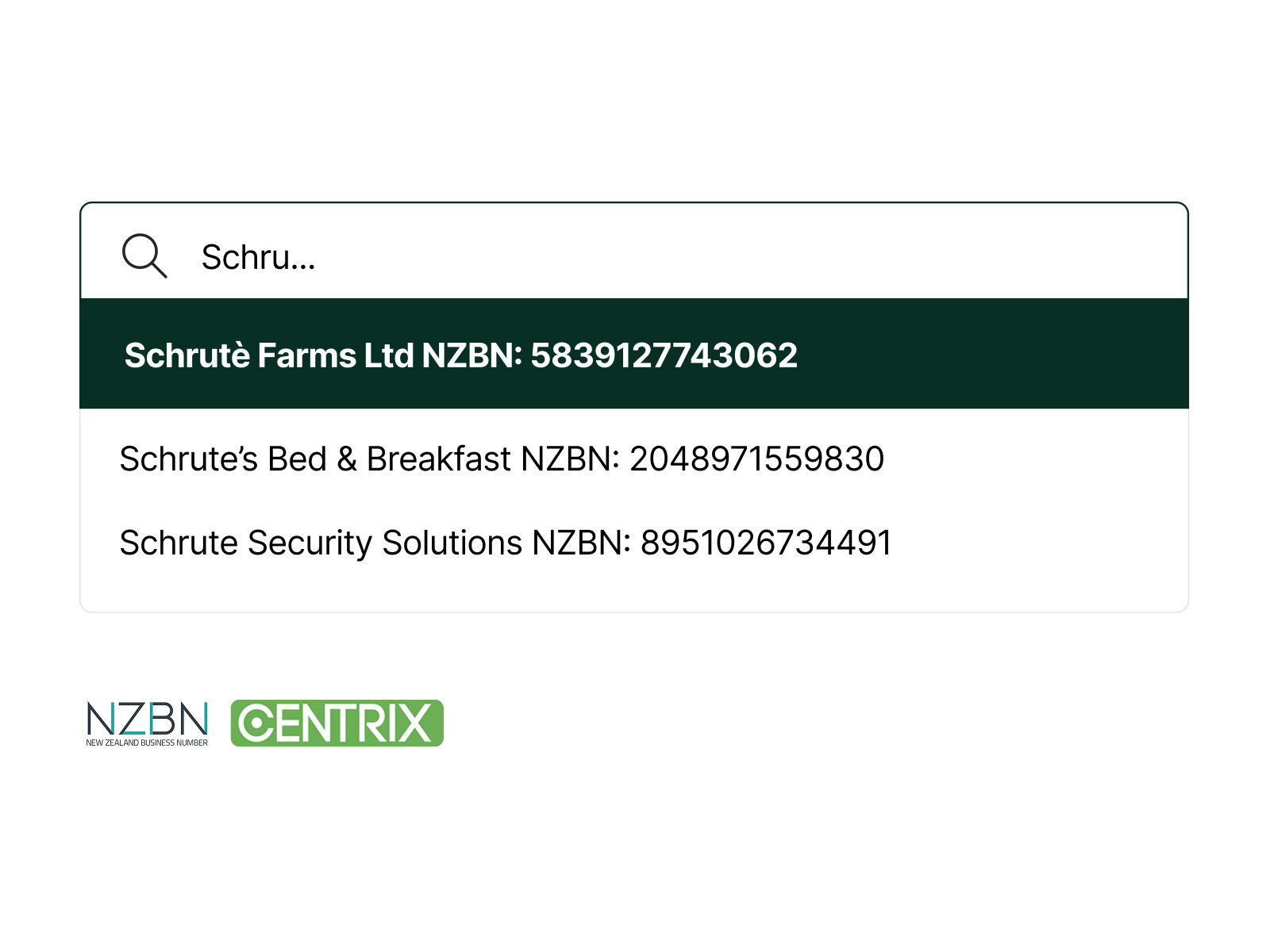

PaidTerms runs a quick automated business check using NZBN and Centrix data to confirm the buyer's details and approve the transaction — typically in seconds.

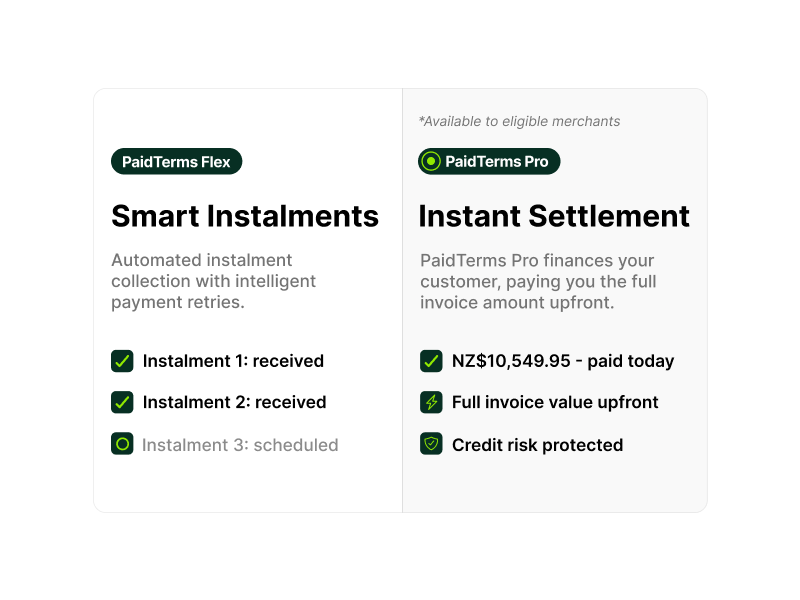

Choose how payment works for your business — both options keep your customer on a clean instalment plan.

Example: Cosmetics Production Order Using Instalments

See how the same scenario plays out differently

Buyer Type

Independent skincare brand placing their first full production run with a contract manufacturer

Order Size Needed

$35,000 across four SKUs to meet minimum batch quantities

- Brand can only afford two SKUs at minimum batch size

- Manufacturer loses half the production order value

- Brand launches with an incomplete range, limiting retail traction

- Manufacturer risks losing the client to a more flexible competitor

- Brand commits to the full $35,000 run across all four SKUs

- Pays in manageable instalments as their product reaches market

- Manufacturer receives $35,000 upfront

- Brand launches with a full range, driving stronger retail and repeat orders

FAQ For Skincare & Cosmetics Manufacturers Offering Instalments

Instalment payments allow your wholesale customers, such as retailers, beauty clinics, pharmacies, distributors, and eCommerce brands, to split large product orders into instalments, typically over 3, 6, or 9 months. The buyer selects an instalment option at checkout or invoice stage and pays over time, while you receive the full invoice amount upfront. This allows you to offer flexible payment terms without extending credit internally or carrying receivables on your balance sheet.

Yes. Offering instalments is well suited to wholesale restocking orders, seasonal product launches, new range rollouts, private label manufacturing, and distributor onboarding. It enables buyers to secure inventory and commit to larger orders without paying the full amount upfront, helping manufacturers increase order size while protecting brand positioning and margins.

Yes. With instalment payments, the manufacturer is paid upfront and in full once the transaction is approved. The customer then repays PaidTerms over time. This structure improves cash flow, reduces debtor days, removes receivables from your balance sheet, and decreases reliance on extended trade terms.

Instalment payments are designed to reduce credit risk for manufacturers. PaidTerms assesses the buyer and manages repayment collections. Repayment risk is held by PaidTerms rather than the manufacturer. This means you are not responsible for chasing overdue invoices or absorbing bad debts.

When buyers can spread payments over time, they are more likely to commit to larger restocking orders, trial new product ranges, and support seasonal launches. Payment flexibility reduces upfront capital constraints and shortens sales cycles. Instead of discounting to secure distribution, manufacturers can use flexible payment terms as a strategic advantage to increase average order value and improve conversion rates.